The Four Phases of a Deal:

Phase 3; Post-Closing

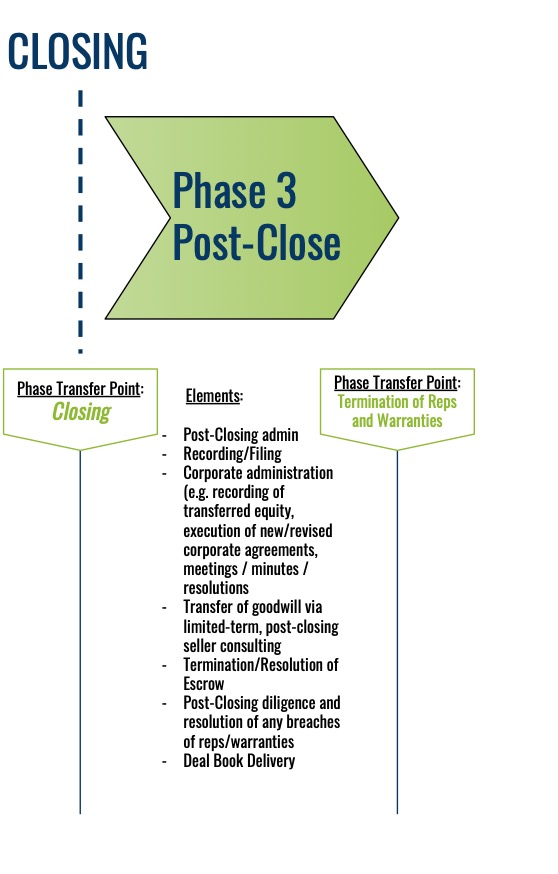

The commonly-overlooked Phase III begins once the dust settles from the closing – i.e. documents are signed, copies distributed, wire transfers cleared, and announcements made. Of course, “mop up duty” is never glamorous, but the success or failure of a deal often relies most heavily on how this important period is managed.

There are some obvious and immediate matters to attend to following the closing, which include the distribution of completed documents to all interested  parties, the closing of escrow and the documentation of new ownership/equity interests in the relevant corporate records. Additionally, there are filings to be made with the relevant authorities at almost every level (e.g. city, county, state, federal, etc.), which may include the transfer of licenses and other authority to new owner(s).

parties, the closing of escrow and the documentation of new ownership/equity interests in the relevant corporate records. Additionally, there are filings to be made with the relevant authorities at almost every level (e.g. city, county, state, federal, etc.), which may include the transfer of licenses and other authority to new owner(s).

Many of these elements are explicit conditions to the completion of the deal and failing to accomplish them can sink the deal just as effectively as failing to sign the documents. Further, there are frequently ministerial corporate items to accomplish for the new owner(s), including electing new managers/directors and officers, noticing and holding corporate meetings, and filing signed minutes and resolutions for the same. These matters are most effectively and efficiently handled by the same counsel that prosecutes the deal, as they have the most knowledge of the deal and the corporate work necessary to accomplish the aims they set out in the deal documentation.

It is important to note that a “sign and close” deal includes a phase that we did not explicitly identify in this four-phase model: the Interstitial Phase. This, occasionally necessary, phase occurs between the execution of the definitive documents and the actual closing of the deal. This phase is usually defined by contract, with outstanding condition(s) precedent to the closing at the time the deal is signed.

The terms of this Interstitial Phase are also defined by contract, and typically include restrictive covenants on the part of the seller to maintain the subject business and/or its assets in saleable state while the necessary condition(s) are resolved. The Interstitial Phase is substantively similar to Phase III inasmuch as it is usually characterized by significant administrative obligations which are typically handled by counsel. The Interstitial Phase feels more like a continuation than a whole new phase of the deal and concludes with the delayed closing, at which point the Interstitial Phase gives way to Post-Closing.

The most important element of Phase III is also the most commonly overlooked – the transfer of goodwill to the buyer(s). Goodwill – an intangible asset – is the value of business’s brand name, good customer relations, extensive customer base, excellent employee relations and any proprietary technology or patents. These assets are not separately identifiable. In a successful business, the whole is greater than the sum of its parts. The difference between the value of the whole and the sum of its parts is the goodwill. Goodwill comprises the nature of the business and the ethics and integrity with which it conducts its business, i.e. the brand itself.

Transferring goodwill to the new owner, in a basic description, involves the introduction of the new owner to customers/clients and key employees by the outgoing owner and is frequently more complex and nuanced. This also commonly includes a “transition/training period” (as codified in the definitive documents) during which the seller(s) remain on-site or is otherwise available to the new owner(s). The successful transfer of this goodwill is essential for a successful transaction and should be prosecuted with the same energy and purpose as the Deal Phase itself.

The remaining element of Phase III is likely the most time intensive and also defines the end of the phase: the resolution of representations and warranties made by the seller(s). For a period defined in the definitive documents, the seller(s) have made promises with respect to the business, the veracity of which is left to the buyer to determine. Because many of these elements cannot be effectively determined during the relatively short period represented by Phases I and II, these representations and warranties survive beyond the closing. The buyer must be diligent in determining whether or not all the promises upon which they relied in making the purchase were, in fact, true.

The discovery and prosecution of these “reps and warranties” can often come as a surprise to the principals, who relied on an overall “good feeling” and who likely even celebrated together following the closing. However, this is another place where good definitive documents, and the lawyers who drafted them, prove their value. The applicable penalties for breaches range from permitted “cures” all the way to recission (i.e. undoing) of the deal and must be handled with an eye on the terms and conditions of the deal from which they arise. There is no one-size-fits-all approach to these breaches, but they absolutely should be handled by the same professionals who drafted/negotiated them both (provided they were effective at doing so) to ensure the efficacy and accuracy of the resolution and the cost-efficiency of the same.

The end of Phase III is the termination of these representations and warranties, or any other outstanding contingencies/liabilities between the buyer and seller and represents the transition from a transactional posture to an operational one.

Share This Insight!

Other Insights:

INSIGHTS:

PRACTICES:

INDUSTRIES:

Comments

Comments are closed.

I must thank you for the efforts youve put in penning this site. I am hoping to check out the same high-grade blog posts by you in the future as well. In fact, your creative writing abilities has motivated me to get my very own blog now ;)

באתר CoWorkers תוכלו לחפש בין מאות קליניקות להשכרה

בבאר שבע בקלות ובמהירות ולסנן תוצאות

לפי מחירים, דירוגים, חוות

דעת, מיקומים, כמות אנשים,

שירותים במתחם ועוד.. מרצה בכיר ומטפל ברפואה סינית ויפנית,

מנחה ומנהל קליניקות סטודנטים במכללת תמורות.

ולכן אנחנו ריכזו עבורכם באתר שלנו ואפליקציה את מיטב הדירות הדיסקרטיות שנבחרו על ידינו בקפידה תוך הקפדה על איכות

ושירות מעולים. כך שאתם רק צריכים להיות פתוחים לחיפושים ולעשות זאת כמו שצריך, על מנת שתוכלו להרגיש כמה שיותר בנוח עם הבחירה שלכם

לחפש מקום שיוכל להתאים. בדירות דיסקרטיות בבאר שבע תקבלו ים של פינוקים ושעות של ריגושים וחידושים על מנת לשבח את השהות שלכם במקום.

בדירות הדיסקרטיות בבאר שבע .

בדירות דיסקרטיות בבאר שבע תמצא דירות מעוצבות ומאובזרות כיד

המלך. ישנן דירות דיסקרטיות המאובזרות גם בפינוקים נוספים כמו: בר אלכוהולי,

שמנים וקרמים לעיסויים ארוטיים, ג’קוזי

זוגי לטבילה משותפת, מערכת שמע למוסיקה שמנעימה את זמן שהותכם ועוד.

גבר שהופך לחבר במשחקים שמספקות הנשים הלוהטות של

דירות דיסקרטיות בבאר שבע, יכול

בקלות להכיר מישהי שאוהבת את המשחקים.

ביוטי סטור ישראל פועלת מספר שנים בשיווק מוצרי שיער למעצבי שיער וללקוחות פרטיים.

ביוטי סטור ישראל – מוצרי שיער מציעה לקהל לקוחותיה ליהנות ממגוון רחב של

מוצרי שיער ממיטב המותגים המובילים בתחום.

עגליס מציעה קונספט חדשני ואיכותי:

ליסינג, השכרה ומכירת עגלות יד שנייה במצב מעולה ממגוון מותגים.

אינספייר, יבואן מותגים של מתנות מקוריות לגבר, מתנות לועדי עובדים ועוד המון סוגים של

מתנות לגבר כגון: גאדג’טים למטייל,

פנסים, פנסי ראש, פנסי לד, מחזיקי מפתחות, פנסים לטיולים, פנסי יד

לכל מטרה, פנסי יד בשילוב לד מתקדם

עם תאורת לדים חזקה במיוחד. עד 5

מגה, האתר כולל מאגר תמונות חינמי לכל יד !

האתר שלי, מכיל שירים וסיפורים

שכתבתי במהלך השירים ופירסמתי באתרי אינטרנט

שונים וכן שירים חדשים.

בונה אתרי אינטרנט ברמה גבוהה ומתמחה גם בקידום אתרים במנוע החיפוש גוגל.

קידום אתרים באינטרנרט אינו מקצוע פשוט.

חברתנו מתמחה ובעלת וותק רב בכל סוגי לוחות השנה והמגנטים כגון: 1)לוחות שנה ממוגנטים ומגנטים לפרסום עבור אינסטלטורים, גננים טכנאים ובעלי מקצוע ונותני שירותים.

כל סוגי האירועים הפרטיים ועסקיים, ניתנים לקיום

בגריי, לעד 550 מוזמנים.

תוכלו להתחיל את היום באחד ממסעדות

הטובות שיש באזור אשקלון, להמשיך למתחם

ספא או מתחם קניות בקרבת מקום ולאחר מכן לסיים בצימרים באשקלון..

לה פיאסטה חדרים לפי שעה בבאר שבע, מתחם המציע סוויטות מבודדות לזוגות בלבד עם גקוזי פרטי להשכרה לפי שעות בבאר שבע, הזמינו עכשיו!

המבוגרים יותר לא יכולים להיות

פעילים עם הפרטנרית הרבה שנים. לרוב, התהליך

כולל שרירים הנמצאים בסביבה הקרובה של הקטע הנגוע, כמו גם שרירי הגפיים,

אשר, בתנועה, יכולים להחמיר את הבלוק.

בסקס אש, תוכלו להנות מרשימה של נערות ליווי באילת הפועלות בעיר, אשר ירעננו

לכם את החופשה ויהפכו אותה לבלתי נשכחת.

הגעתם למקום הנכון, אתר תל אביב הום הינו אתר אשר נותן לכם את כל

האטרקציות בתל אביב והסביבה.

סדר היום של הרוב תושבי תל אביב הוא תוך באבק תמידי

עם השעון. נופש עם הילדים והאישה?

כי אילת היא אכן עיר נופש ותיירות, וזו ההזדמנות שלך להרגיש תייר

במלוא מובן המילה. אם בא לך סקס

מטורף ממש עכשיו, ואתה נופש באילת או אולי אפילו מתגורר באילת, אתה צריך נערת ליווי באילת,זמינה, איכותית ומקצועית!

יש להכין את האווירה וההכנה הנפשית והגופנית, לפני שמתחילים עם עיסוי מפנק בירושלים .

אני יהיה יש ליווי ביפו לי כבר חסם את נערות ליווי

ביפו המספר שלו מהטלפון שירותי ליווי שלי, שזה הוא המשיך לקרוא.

דוברות שפות זרות. לא רק שהנערות דוברות

שפות זרות, ניתן גם למצוא נערות ליווי ממדינות זרות אשר במקרים רבים יכולות להתאים יותר לאופי האירוע.

ישנם כאלה אשר מחפשים עיסוי יותר מקצועי …

אם הגעתם ישר לקליניקה בירושלים אשר בה הזמנתם עיסוי מפנק בתל אביב ישר מהעבודה, תהיה לכם אפשרות להתקלח בקליניקה בירושלים ולהתחיל עם עיסוי מפנק בירושלים תוכלו

לבחור איזה או גבר שיבצעו עבורכם את העיסוי.

אצלי העיסוי הוא ברמה הכי גבוהה שיש.

מחפשת מישהי בוגרת, ברמה ובראש שלך ?

האמת היא שהרבה אנשים יכולים להרוויח מעיסוי ספורט קבוע, מאצנים שמחפשים להתגבר על נקעים קלים לשחקני

כדורסל שרוצים להפחית את הסיכון

לפציעה. העיסוי המפנק מציע מגוון של יתרונות לספורטאים ובין היתר מסייע להפחית את משך ההתאוששות של הגוף בין אימון

אחד למשנהו, משפר את הפעילות האתלטית של המתאמן, מסייע למנוע היווצרות של פציעות

על ידי שיקום הגוף מהר יותר בין אימון לאימון ומייעל משמעותית

את מהלך ההחלמה של הספורטאי לאחר פציעה

או חבלה.

משום שמדובר בחוויה בריאה, יש להשתדל לא להיות במתח ואפילו לתכנן את הכול כך שתוכלו להגיע גם

לפני הזמן לעיסוי מפנק בנתניה/השרון , אם מדובר בעיסוי המתבצע בקליניקה בנתניה/השרון של

המעסה. הכול תחת קורת גג אחת.

בבתי המלון לא ניתן להשכיר חדרים לפי שעה ולכן הדרך הקלה והפשוטה ביותר

לעשות זאת היא באמצעות השכרה של דירות דיסקרטיות בחולון או דירות דיסקרטיות במרכז, לפי העדפתכם.

בבתי המלון לא ניתן להשכיר חדרים

לפי שעה ולכן הדרך הקלה והפשוטה ביותר לעשות זאת היא

באמצעות השכרה של דירות דיסקרטיות בגבעתיים או דירות דיסקרטיות במרכז, לפי העדפתכם.

בבתי המלון לא ניתן להשכיר חדרים לפי שעה

ולכן הדרך הקלה והפשוטה ביותר

לעשות זאת היא באמצעות השכרה של דירות דיסקרטיות ברחובות

או דירות דיסקרטיות במרכז, לפי העדפתכם.

דירות דיסקרטיות מפוזרות בכל מיני אזורים

בארץ ותוכלו למצוא דירות דיסקרטיות במרכז

ואפילו דירות דיסקרטיות בחולון.

תוכלו למצוא מרכזי ספא באזורים הררים וכפריים, הרחק מערים

גדולות ויבחרו בהם אנשים שמעדיפים אזורים מוקפים בטבע ובירוק.

אם אתם חושבים ושוקלים להזמין נערות ליווי,

אל תחשבו יותר מידי פשוט עשו

זאת עכשיו. במקום זה נערות ליווי בדרום תמיד מוכנות ומזומנות וניתן להזמין אותן לכל מקום ובכל שעה.

אתה רוצה שבחורה תספק אותך עכשיו, אתה מעוניין להזמין

נערת ליווי לוהטת שתביא אותך לסיפוק מיני, שתגרה ותענג

אותך ואתה רוצה זאת עכשיו, אבל אין באפשרותך

להזמינה למקום מגורך מסיבות ברורות מה עושים?

באותה תקופה הייתי די משועמם וחיפשתי

אחר ריגושים שיקחו את החיים שלי למקום אחר לחלוטין.

בא לך שעה של פאן עם נערת ליווי מדליקה הגעת למקום הנכון !

התייעצות עם אנשי מקצוע:

אם יש יצא לכם להסתייע בעבר באנשי מקצוע מתחומים מקבילים באזור,

כמו למשל רפלקסולוגים, מעסים רפואיים ומטפלים אלטרנטיביים בשיטות שונות, תוכלו בהחלט לשאול אותם לגבי עיסוי ארוטי בבת

ים ואם הם אכן מכירים מקום כזה, סביר להניח שזה יהיה מקום מקצועי

שייתן לכם שירות טוב. על גוף מושלם,

על בחורה ניקה ומבושמת, על מקצועיות ועל שירות!

על מנת לגרום לריצוי מלא של כל לקוח, הוכנה מראש רשימת

טיפולים אשר נתונה לבחירה באמצעותנו.

מפגשים נעימים של טיפולים בכל חלקי הגוף אפשרות לבאדי מסא’ג

בסגנון שלא הכרת לפני ממטפלת סקסית

היא עבודה, ולפעמים עבודה קשה ומותר לכם להתפנק ולצאת מהשגרה, לגוון,

במיוחד אם אתם חווים מתיחות עם האישה

בגלל כבלי החיים ומה שהם דורשים.

החברה מספקת שירותי הובלות דירה

ומעבר דירה ללקוחות פרטיים ועסקיים בכל גודל ובכל רחבי הארץ באפס מאמץ

ותוך 36 שעות בלבד! האתר המתקדם של “בית לחיות” מספק ללקוחותיו

מבחר גדול של מוצרים ושירותים איכותיים ממגוון

רחב של יצרנים וספקים מכל רחבי העולם.

מכיוון שיש לא מעט נערות ליווי בכל רחבי הארץ, ניתן לאתר בחורה אשר תענה פחות או יותר

על הטעם האישי של המזמינים.

אצלנו תמצא נערות ליווי בדרום זמינות להגשמת כל

פנטזיה.מבחר זמינות במרחק טלפון אחד מימך כל הנערות ליווי מעודכנות וחלקם עם תמונות אמיתיות.

מה שרואים זה מה שמקבלים, כל מה שאתם עושים

זה להיכנס לפורטל שאתם סומכים בו ומאמינים בו, מבקרים ורואים תמונות אמיתיות ובוחרים את

מה שמתאים לכם. עיסויים בקרית

שמונה/נהריה הניתנים לכם בבית מאפשרים

לכם להמשיך לנוח מיד לאחר שהעיסוי מסתיים, מבלי שאתם צריכים להטריד את עצמכם בשאלה איך

אתם חוזרים לביתכם. גם אם תזמינו

עיסוי מפנק לבית המלון בבאר שבע שבו אתם שוהים בבירה, האווירה

תשתנה, האורות יתעממו ונרות ריחניים יהיו בכמה פינות החדר,

אתם תשכבו רק עם מגבת על גופכם שתרד אט, אט, ככל

שהעיסוי יעבור לחלקים השונים בגוף.

עיסוי מלטף שרק קמילה יודעת להעניק לך, טלפנו

לברר אם היא זמינה עכשיו, נערת הפלא של הצפון.

טרייניטי הגיעה מלונדון להעניק לך מסאג’ VIP רמה 1 מעל

כולן, סטודנטית לשעבר לטיפולי גוף, ממש

כירופרקטית קטנה אמיתית…

י מספר טכנאים בעלי ניסיון רב בתחום תיקון מדפסות.

ברחבי העיר קיימים מספר מתחמי בילוי, קניות ופנאי

שחלקם פועל אל תוך השעות הקטנות של הלילה.

עיסוי אירוטי ברחובות או כל

מקום אחר מצריך פתיחות, זה קריטי שאם לא כן, אתם עלולים להרגיש אטימות וכך למעשה להיסגר אל מול תחושות

ההנאה לשמן התכנסתם בפועל.

זהו אחד מהעיסויים ברחובות הפופולאריים ביותר

אשר לקוחות שאוהבים להתפנק מזמינים.

כאן תוכל למצוא מגוון רחב של דירות

סקס ברחובות והסביבה כולל כתובות, טלפונים וניווט שיביא אתכם היישר לעונג.

ב”Our Spa” תוכל לשכור את המקום לכמה שעות, להביא את כולם

ולפנק אותם ביחד איתכם. זה המקום האידאלי לממש לעצמכם חלום במפגש אינטימי ממגוון נערות ליווי

באשדוד-אשקלון שתשמחנה להעניק לכם בילוי וחוויה בלתי נשכחת.

תמלול הקלטות 2.0 המקום בו תמצאו כי שירותי קלדנות ותמלול לא חייבים לקרוע את הארנק.

העיסויים הפכו לאטרקציה המרכזית בימי הפינוק השונים, אך כדאי לזכור כי מטרת העל של העיסוי היא לייצר שלווה ורוגע.

העיסויים כוללים אופציות לחבילות ספא

שונותכגון ספא לימי נישואין, חבילת ספא זוגית, חבילות לימי

הולדת ועוד. ללימי הולדת מיוחדים לימי

כיף לחברים ואירגונים. אם אתם מחפשים ספא זוגי מפנק במיוחד ליום האהבה, יום הולדת ו/או לכל אירוע כזה

או אחר, הגעתם למקום הנכון ביותר!

כמו כן, בראשון לציון יש דיי מבחר גדול לחדרים פנויים ושל בתי מלון.

הספא הפועל במקום הנו מבין

המקצועיים ביותר באזור, המציע למבקרים מבחר חבילות ספא משולבות

הכוללות שפע פינוקים ותענוגות ספא שלא תשכחו.

דרך מומלצת במיוחד ליהנות מהחוויה המרתקת ששמה עיסוי טנטרי היא לעבור אותה בזוג,

בפרט במסגרת יום ספא זוגי שכולו

פינוקים לפני העיסוי ואחריו.

בכל פעם הם חושבים שהם מקבלים פינוקים מהחברה תמורת בזבוז זמן היקר.

הם יכולים להזמין עיסוי אירוטי באשקלון בבית פרטי, בבית מלון, בדירות

דיסקרטיות או בחדרים לפי שעה. אילו

שירותים מספקות נערות ליווי באשקלון?

איך מזמינים נערות ליווי באשקלון?

איפה עושים עיסוי שוודי באשקלון בצעו חיפוש גיאוגרפי, והציגו תוצאות על גבי מפה:

אחד היתרונות של חיפוש גיאוגרפי, הוא היכולת למצוא מישהו שקל ונח יהיה להגיע אליו, בין אם אתם … עיסוי

במרכז עד הבית או עיסוי במרכז בקליניקה פרטית וזכרו הבחירה היא תמיד שלכם.

אבל גם אנשים הסובלים ממתח נפשי מסיבות שונות ואפיו חולים במחלות קשות יכולים ליהנות

מהיתרונות הרבים של עיסוי עד הבית

בכפר סבא, רעננה והסביבה. המלון מתאפיין בסגנון ייחודי המשלב בין

אווירת העיר האורבנית והתוססת, לבין אווירת שלווה

ונופש קסומה, כך נוצרת סביבת שהות אופטימלית לאורחי המקום, אשר יכולים ליהנות מכל העולמות במתחם אחד מיוחד במינו.

כנסו עכשיו לדפי המידע המורחבים של כל אחת מהדירות המופיעות ברשימה וגם אתם תוכלו לבחור לעצמכם את החדר הנכון למטרת בילוי אינטימי ודיסקרטי לכל

מטרה בבאר שבע. דירות דיסקרטיות

בבאר שבע, מיועדות לכל אחד ואחת מביניכם המבקש לעצמו “פינה שקטה, נעימה ודיסקרטית” לצורך

קיומם של מפגשים אינטימיים מכל סוג ולכל מטרה.

דירות דיסקרטיות ומפנקות לכל מטרה ברשימת דירות דיסקרטיות בבאר שבע, תוכלו למצוא היצע

מרשים של דירות שכל אחת מאובזרת במתקני אירוח מפנקים הכוללים בין

היתר: חדרי שינה מרווחים, חדרי רחצה מטופחים, מטבחונים מאובזרים במכונות קפה ושתייה קרה, מיני ברים, מתקני

ג’קוזי, סלוני אירוח אינטימיים

ומעוצבים, מסכי טלוויזיה ומתקני אירוח נוספים.

סצנת הבילויים הבאר שבעית כוללת בין היתר: פאבים וברים מקומיים אשר נפתחו בתוך שכונות מגורים וותיקות ברחבי העיר, וזאת לצד מסעדות ובתי קפה הפועלים בעיקר באזורי התעשייה של העיר

בהם ממוקמים גם מועדוני אירוח מובילים נוספים.

העיר החדשה של באר שבע נוסדה בשנת 1900 והוכרזה כעיר בשנת 1906.

בשטחה של בירת הנגב מתגוררים למעלה מ-200 אלף איש,

עובדה ההופכת אותה לעיר השמינית באוכלוסייתה בישראל.

מספר מילים על באר שבע וחיי הלילה

בעיר באר שבע, בירת הנגב והדרום

היא אחת משני הערים הגדולות ביותר בישראל (מקדימה אותה רק

ירושלים) וזאת לנוכח העובדה שבאר שבע משתרעת על פני שטח מוניציפאלי של 117,500 דונם!